A Deep Dive into PCI Compliance Questionnaires: Understanding the Differences and Overcoming Challenges

Payment security is critical in today’s digital economy, and the Payment Card Industry Data Security Standard (PCI DSS) plays a vital role in protecting payment card data from breaches and fraud. However, achieving PCI compliance can feel overwhelming, especially when organizations must determine the correct Self-Assessment Questionnaire (SAQ) or PCI compliance questionnaires to complete.

This article will provide a detailed breakdown of the different PCI DSS SAQs, the challenges businesses face in completing them, and best practices to streamline compliance. We’ll also explore risk appetite statements, clarify the roles of Qualified Security Assessors (QSAs) and Approved Scanning Vendors (ASVs), and conclude with a call to action for expert PCI compliance guidance.

What are PCI Compliance Questionnaires?

PCI compliance questionnaires are a set of self-assessment tools designed to help organizations determine whether they meet PCI DSS requirements. These questionnaires are part of the larger PCI DSS compliance process, which includes other activities like conducting vulnerability scans and performing security assessments.

Completing a PCI compliance questionnaire helps organizations identify areas where they may not be meeting PCI DSS requirements and provides a way to demonstrate compliance with the industry standard. Depending on the size of the organization, the number of transactions processed, and the complexity of the payment card data environment, you may be required to complete one of several different types of questionnaires.

Understanding PCI DSS Self-Assessment Questionnaires (SAQs)

The PCI DSS SAQ is a validation tool used by businesses to self-assess their compliance with PCI DSS requirements. Not all businesses need the same questionnaire—the appropriate SAQ depends on how an organization processes, stores, or transmits cardholder data.

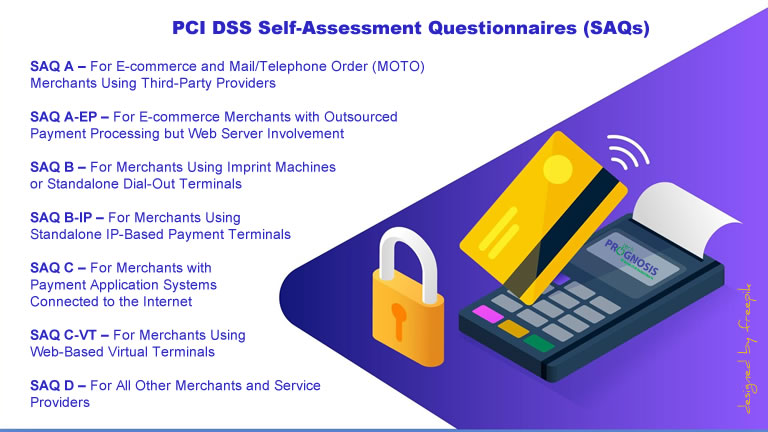

1. SAQ A – For E-commerce and Mail/Telephone Order (MOTO) Merchants Using Third-Party Providers

- Who should use it?

- Merchants that fully outsource payment processing to a PCI DSS-compliant third party.

- No cardholder data is stored, processed, or transmitted on the merchant’s systems or premises.

- Example: A subscription-based e-commerce business that uses Stripe, PayPal, or Adyen for payment processing and does not store credit card information.

- Questionnaire Size: 22 questions.

2. SAQ A-EP – For E-commerce Merchants with Outsourced Payment Processing but Web Server Involvement

- Who should use it?

- Merchants outsourcing payments to a third party but maintaining a website that directs customers to the payment processor.

- Example: A small online retailer whose checkout page redirects to Authorize.net, but their website captures customer information before checkout.

- Questionnaire Size: 191 questions.

3. SAQ B – For Merchants Using Imprint Machines or Standalone Dial-Out Terminals

- Who should use it?

- Merchants that process payments only via imprint machines or standalone, dial-out POS terminals with no electronic storage of cardholder data.

- Example: A small boutique that manually imprints card details for processing later.

- Questionnaire Size: 41 questions.

4. SAQ B-IP – For Merchants Using Standalone IP-Based Payment Terminals

- Who should use it?

- Merchants that only process payments using standalone IP-based POS terminals that are PCI-compliant and don’t store cardholder data.

- Example: A fast-casual restaurant using a Clover or Ingenico POS terminal that connects via the internet but does not store credit card data.

- Questionnaire Size: 82 questions.

5. SAQ C – For Merchants with Payment Application Systems Connected to the Internet

- Who should use it?

- Merchants using a POS system connected to the internet, but not storing cardholder data.

- Example: A hotel using a networked POS system for check-in payments that transmits but does not store card data.

- Questionnaire Size: 160 questions.

6. SAQ C-VT – For Merchants Using Web-Based Virtual Terminals

- Who should use it?

- Businesses processing transactions manually through a web-based virtual terminal with no cardholder data storage.

- Example: A law firm manually entering client payments into a secure virtual terminal like Square.

- Questionnaire Size: 83 questions.

7. SAQ D – For All Other Merchants and Service Providers

- Who should use it?

- Any business that stores, processes, or transmits cardholder data beyond the scope of the other SAQs.

- Example: A large retailer that stores customer card data for subscription billing.

- Questionnaire Size: 328+ questions.

Common Challenges Organizations Face with PCI Compliance SAQs

1. Determining the Right SAQ

Many organizations struggle to identify the correct SAQ, leading to errors and increased compliance risks.

Solution: Work with a PCI compliance expert to ensure correct SAQ selection.

2. Understanding the Technical Requirements

The SAQ contains security-related questions that can be complex for non-technical teams.

Solution: Collaborate with IT and cybersecurity professionals to ensure compliance.

3. Meeting Security Controls Without a Large Budget

Implementing PCI DSS security controls can be costly.

Solution: Use cost-effective security tools like firewalls, endpoint protection, and tokenization to minimize expenses.

4. Keeping Up with PCI DSS Updates

Regulatory updates (e.g., PCI DSS 4.0) require ongoing adjustments.

Solution: Establish a compliance review cycle to stay up to date.

Best Practices for Completing PCI Compliance SAQs

✔ Review Your Payment Processing Flow – Document how your organization handles payment transactions before choosing an SAQ.

✔ Engage a PCI Compliance Expert – A QSA (Qualified Security Assessor) can guide organizations through the SAQ process.

✔ Use Secure Payment Methods – Reduce risk by using tokenization, point-to-point encryption (P2PE), and EMV chip readers.

✔ Maintain Strong Security Policies – Ensure employee training and access controls to protect cardholder data.

✔ Leverage Automation – Utilize compliance management tools to track security measures and generate SAQ reports efficiently.

Sample Risk Appetite Statements for PCI DSS Compliance

Risk appetite statements help organizations define acceptable levels of risk in their payment security.

✅ Low-Risk Appetite: “Our organization has zero tolerance for storing cardholder data. All transactions are processed through PCI DSS-certified third-party providers.”

✅ Moderate-Risk Appetite: “We allow processing of cardholder data only on segmented, monitored, and encrypted networks with strong authentication controls.”

✅ High-Risk Appetite: “We retain customer cardholder data for recurring billing but implement rigorous encryption, monitoring, and access controls.”

QSAs vs. ASVs: What’s the Difference?

Qualified Security Assessor (QSA)

✔ Role: PCI SSC-approved professional that performs PCI DSS assessments and audits.

✔ Example: A QSA conducts an on-site PCI DSS assessment for a retailer storing customer cardholder data.

Approved Scanning Vendor (ASV)

✔ Role: PCI SSC-approved vendor that performs external vulnerability scans for PCI compliance.

✔ Example: An ASV like Tenable or Qualys provides quarterly PCI scans to check for security vulnerabilities.

Which One Do You Need?

- If you process a large volume of transactions or store cardholder data, you may need a QSA assessment.

- If you only need external network scans, an ASV service suffices.

Call to Action: Simplify Your PCI Compliance

Navigating PCI DSS compliance doesn’t have to be overwhelming. Our team of PCI compliance experts can help you:

✅ Identify the correct PCI DSS SAQ

✅ Implement cost-effective security controls

✅ Work with QSAs and ASVs to meet compliance requirements

📅 Schedule a free 15-minute PCI compliance discovery call today!

Final Thoughts

Understanding PCI DSS SAQs, risk management, and security controls is crucial for businesses that process card payments. By following best practices and leveraging PCI compliance experts, organizations can reduce risks, avoid penalties, and build customer trust.

🔍 Need help with PCI compliance? Book your discovery call now!

References

- Payment Card Industry Security Standards Council (PCI SSC) – www.pcisecuritystandards.org

- Visa PCI Compliance Guide – www.visa.com

- Mastercard Security Standards – www.mastercard.us